Receiving calls from a collection agency can feel overwhelming and stressful. Your first instinct might be to pay them quickly to make the calls stop. At A.C. Waring & Associates, we have seen many clients who made hasty payments to collectors without understanding the full implications. Our team of Licensed Insolvency Trustees and credit counselling professionals regularly guides people through these complex situations.

However, paying a collection agency without understanding the consequences can actually hurt your financial situation and will not improve your credit score since the damage has already been done.

Key Takeaways

- Your credit score has already been damaged once the debt goes to collections

- Paying collection agencies will not remove derogatory information on your credit report

- Collections automatically fall off your credit report after 6 years from the last

transaction done in Alberta

- Making payments can reset the statute of limitations on old debts

- Professional debt solutions like consumer proposals may be more effective than paying collections directly

Understanding Debt & Collection Agencies

What Happens When Your Debt Goes to Collections

When you cannot make payments on a debt, the original lender eventually gives up trying to collect. They either sell your debt to a collection agency or hire one to collect on their behalf. Understanding the legal implications of debt in Alberta helps you recognize your rights during this process.

This transfer happens after your account becomes significantly past due. The collection agency then becomes your new contact point for this debt.

How Collection Agencies Get Your Debt

Collection agencies may purchase debts for pennies on the dollar from the original creditor. They profit by collecting more than what they paid for your debt.

Some agencies work on commission instead, keeping a percentage of what they collect. Either way, they have strong incentives to get you to pay quickly. This is why seeking advice from trusted government resources about collection agency practices can protect your interests.

Your Rights When Dealing with Collection Agencies

You have specific rights under Alberta law when dealing with collection agencies. They cannot harass you, call at unreasonable hours, or use threatening language.

You can request written validation of the debt and ask them to communicate only in writing. Understanding these rights helps you take control of the situation.

When Will Lenders Contact Collection Agencies?

Timeline for Debt Collection Referrals

Most lenders send accounts to collections after 90–180 days of non-payment. Credit card companies often wait 120–180 days before taking this step. If you are struggling with overwhelming credit card debt, this timeline gives you opportunities to seek help before collection agency involvement.

Medical debts and utility bills may go to collections faster, sometimes after just 60 days. The timeline varies depending on the creditor’s policies and your payment history.

Types of Debt That Go to Collections

Almost any type of unpaid debt can end up in collections. Credit cards, personal loans, medical bills, and utility payments are common examples.

Government debts, like taxes or student loans, have different collection processes. These debts often have more serious consequences and different resolution options. The Canada Revenue Agency’s collection practices differ significantly from those of private collection agencies.

Warning Signs Your Account May Go to Collections

You will typically receive multiple notices before your debt goes to collections. These warnings give you time to contact your creditor and arrange payment plans.

Missing 2–3 consecutive payments usually triggers collection warnings. Taking action during this window can prevent the more serious consequences of collection agency involvement.

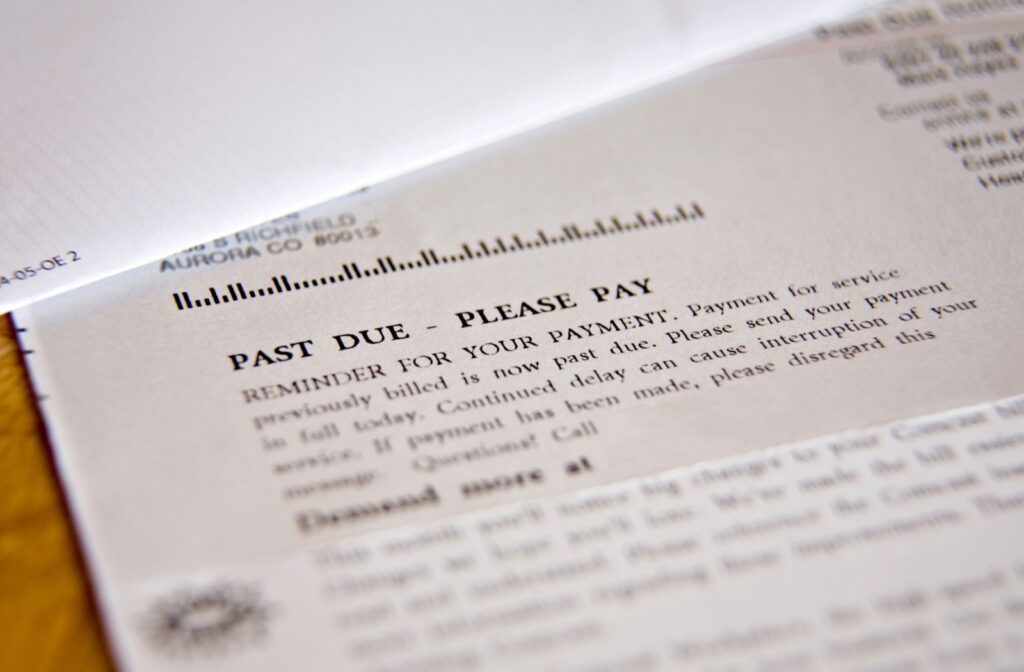

The Hidden Risks of Paying Collection Agencies

How Payments Reset Your Credit Report Timeline

Making any payment on a collection account can restart the clock on how long it stays on your credit report. This means the derogatory notation could remain visible for longer than the standard 6 years.

Even partial payments can trigger this reset. The collection account gets updated as “recently active,” extending its impact on your credit report.

Why Your Credit Score Will Not Improve After Payment

Paying a collection agency does not remove the derogatory information from your credit report. The account simply changes from “unpaid collection” to “paid collection.”

Both statuses have similar negative impacts on your credit score. Lenders still see that you had trouble paying your debts on time, regardless of whether you eventually paid the collection agency. This is why exploring options like debt settlement and its effects on credit scores might yield better long-term results.

The Statute of Limitations Problem

In Alberta there is a two year statutory period, creditors have a limited time to sue you for unpaid debts. Making a payment can restart this limitation period because the two year period is from the last ‘transaction date’.

This means a debt that was previously too old to result in legal action becomes actionable again. You could face lawsuits for debts you thought were beyond collection.

How Do I Pay a Collection Agency Safely?

Getting Proper Documentation Before You Pay

Always request written verification of the debt before making any payment. This documentation should include the original creditor, debt amount, and your payment history.

Do not provide payment information over the phone during initial calls. Legitimate collection agencies will provide written verification when requested. Professional guidance on how to handle debt collection agencies can help you navigate these conversations effectively.

Negotiating Settlement Terms

Collection agencies often accept less than the full amount owed. You can often negotiate a settlement for one half to two thirds of the original debt..

Get any settlement agreement in writing before making payment. This protects you from future collection attempts for the remaining balance. The Financial Consumer Agency of Canada provides guidelines on proper collection agency practices and settlement procedures.

Payment Methods That Protect You

Use payment methods that provide documentation and protection. Bank drafts or certified cheques create clear paper trails.

Avoid giving collection agencies access to your bank account through automatic withdrawals. This prevents unauthorized future withdrawals and gives you better control.

How Do I Get a Collection Removed from My Credit Report?

Understanding the 6-Year Removal Rule in Alberta

Derogatory credit information automatically falls off your credit report after 6 years from the last transaction date which is either the last time you made a payment or the last time you incurred the credit privilege. This happens regardless of whether you pay the collection agency.

Making payments to collection agencies may or may not restart this timeline. Learning about your credit report, score, and rating helps you understand how these timelines work.

When Collections Fall Off Naturally

You do not need to take any action for derogatory credit information to be removed after 6 years. The credit reporting agencies automatically delete these entries.

Sometimes the removal does not happen exactly on schedule due to administrative delays. You can contact credit reporting agencies for timely removal after the 6-year period expires. Equifax and TransUnion Canada are the main credit bureaus that maintain these records.

Legal Ways to Remove Collection Accounts Early

You can dispute collection accounts that contain errors or inaccuracies. Successfully disputed items may get removed from your credit report within 60 days of your dispute communication if determined to be valid.

Some collection agencies will agree to remove the account in exchange for payment, called “pay for delete.” However, this practice is not guaranteed, and many agencies refuse these arrangements.

Better Alternatives to Paying Collection Agencies

Credit Counselling Options

Non-profit credit counselling services help you understand your options without the pressure to pay immediately. These services provide unbiased advice about handling collection accounts. Our credit counselling services focus on education and sustainable debt management strategies.

Credit counsellors can help you create budgets and negotiate with creditors. They offer education and support without the financial conflicts of interest that collection agencies have.

Consumer Proposals in Alberta as a Solution

Consumer proposals allow you to settle all your debts, including ones in collection, for less than you owe. This legal process stops collection calls and provides an improved financial situation.

Licensed Insolvency Trustees administer consumer proposals, facilitating fair treatment for both you and your creditors. This option often costs less than paying collection agencies individually.

When Licensed Insolvency Trustees in Edmonton Can Help

Licensed Insolvency Trustees provide comprehensive debt solutions beyond just bankruptcy. They can evaluate whether paying collection agencies makes sense in your specific situation.

These professionals understand the long-term consequences of different debt repayment strategies. Their advice considers your entire financial picture, not just individual collection accounts.

Bankruptcy Solutions in Alberta for Situations of Overwhelming Debt

Bankruptcy eliminates most debts, including collection accounts, when your financial situation is overwhelming. This legal process provides protection from collection action and a path to financial recovery.

While bankruptcy has certain limited consequences, it may be preferable to struggling with multiple collection agencies for years. Licensed Insolvency Trustees can help you understand whether bankruptcy is appropriate for your situation. Our bankruptcy services provide compassionate guidance through this difficult process.

Making the Right Decision for Your Financial Future

Factors to Consider Before Paying Collections

Consider how old the debt is and how much time remains before it falls off your credit report naturally. Paying collections on debts that will disappear soon rarely makes financial sense. Furthermore, always remember the business of the two year statute of limitations in Alberta which precludes court action after that date.

Evaluate your overall debt load and ability to pay other obligations. Paying one collection agency while ignoring other debts does not improve your financial stability. Trustees will help you create a comprehensive debt repayment plan to address all your obligations systematically.

When Working with Licensed Insolvency Trustees Makes Sense

If you are dealing with multiple collection agencies or overwhelming debt, professional help often provides better results than paying collectors individually. Licensed Insolvency Trustees offer legal protection and comprehensive solutions.

These professionals can stop collection calls immediately through legal processes while helping you address all your debts systematically. The Office of the Superintendent of Bankruptcy regulates these professionals to ensure they meet strict standards.

Your Path Forward with Professional Debt Relief

Do not let collection agencies pressure you into hasty decisions that could hurt your financial future. Take time to understand your options and get professional advice.

At A.C. Waring & Associates, we understand the stress of dealing with collection agencies because we have helped countless people navigate these challenging situations. Contact us for a free consultation to explore debt relief options that can improve your financial situation rather than just satisfying collection agencies.